Award-winning PDF software

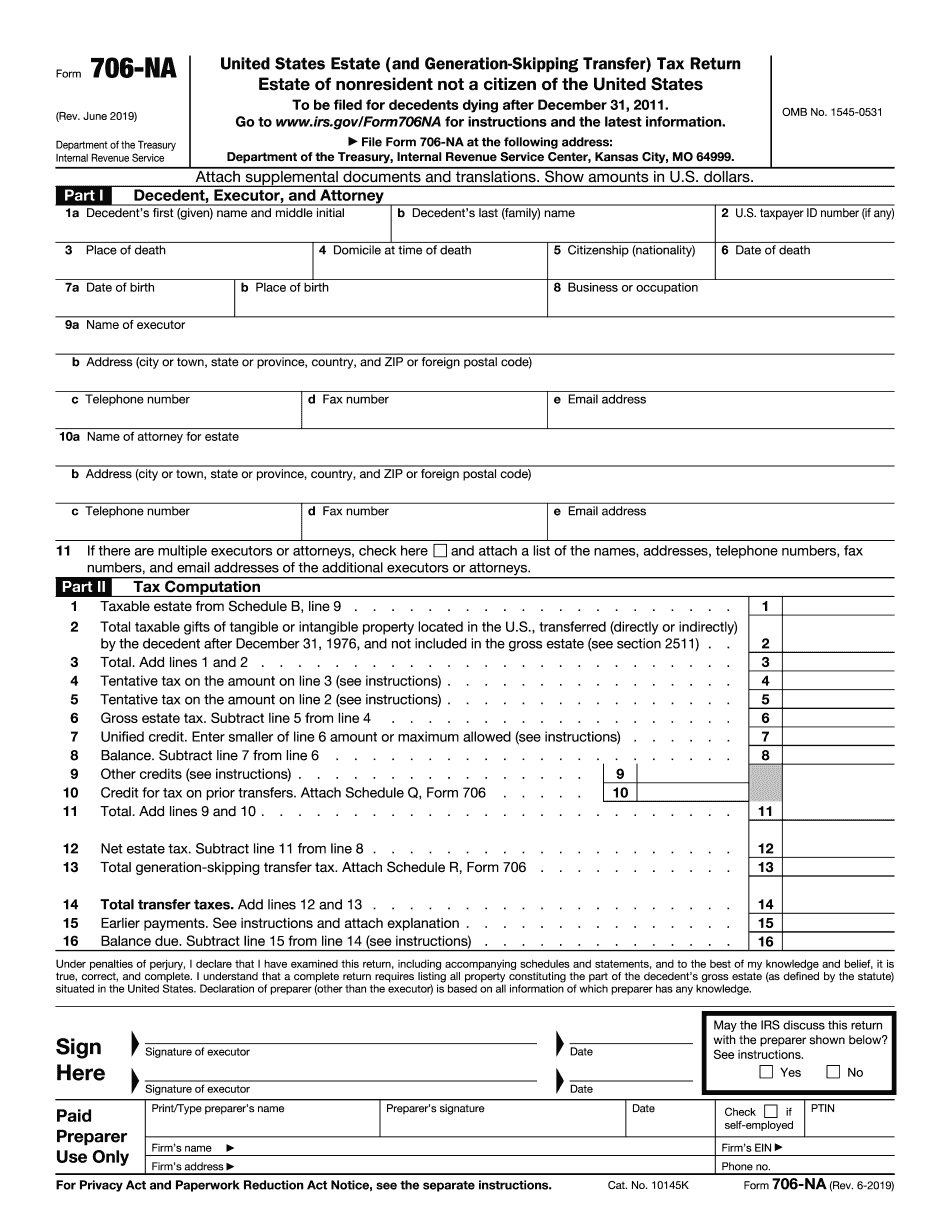

About form 706-na, united states estate (and generation-skipping

See the section of the form for complete details.

form 706-na (rev. june ) - internal revenue service

Rev. Jan. 2015). Nonresident's nonresident estate tax return based on estate law provisions. (Jan. 2018). Resident's nonresident estate tax return based on estate law provisions. (Jan. 2018). Estate / Donor Deductions. See Pub. 575. In addition to the other deductions allowed in chapter 4, you may deduct contributions you make or receive to a social welfare organization on Form 1040 or Form 1040NR. You cannot deduct contributions you have received for a child for an amount later transferred to the beneficiary's estate. See chapter 11 for specific rules on the amount of contributions. If you give up your right to make gifts to a designated person (such as grandchildren) or to make a gift of your home, you may deduct the value of the gift on Form 706. If you give up your right to make gifts to a designated person for a period of time under a non-qualified deferred.

Form 706-na definition - investopedia

The IRS defines nonresident aliens as “persons who do not meet the requirements under subsection 3(1) of the Act, as amended (the Act), for being a resident alien for income tax purposes” (, foreign countries, territories, and possessions except the Virgin Islands). Nonresident aliens are taxed using the same rules as residents to whom the same laws apply. Taxpayers who do not qualify as foreign nationals (including in the context of the nonresident alien generation-skipping transfer) must complete a return and provide all information as required by the IRS, including a completed W-4 form, the required Schedule D with all appropriate schedules on which to itemize other deductions and credits, and an attached income tax filing instruction. The IRS will not provide advice or provide you with a written or phone explanation of the instructions. Therefore, we suggest that taxpayers complete a Form 706-NA. Taxpayers who wish to file a Form.

Filing form 706-na to secure an transfer certificate form 5173

PM.

The deceptive simplicity of us form 706 na - us estate (and

This is a critical question to check. If decedent is not living in the US, but is the beneficiary or inheritor of decedent's US property, then it will often include a “US real property interest” which generally will be a personal residence. To determine the US real property interest, you need: First, determine which US income tax rate applies to the assets the real property interest is in. For example, if the US capital gains tax rate is 20), then the real property interest is effectively taxed to the decedent since that tax rate applies to an additional US income tax rate of 28). The easiest way to determine whether the real property interest is subject to the 20% US capital gains tax is to compare the decedent's original tax bracket. The table below shows the decedent's adjusted gross income from each of his 10 tax years (in order of tax.