Hi, if you're here, that means you're probably wondering about some of the pitfalls of federal portability when it comes to estate tax planning. There are a number of pitfalls of relying on portability that I want to cover for you quickly. One of the most common pitfalls we see with portability is that it doesn't apply to Minnesota state taxes. Portability is only a federal thing, so it doesn't apply to Minnesota. Minnesota has a much lower estate tax exemption of only a million dollars. So, if your state is at or anywhere near a million dollars in total estate tax value, you're going to need to do some planning here to double the amount of the exemption. In Minnesota, portability won't help you. Another issue we see with portability is that it doesn't provide any asset protection for a surviving spouse in the way traditional trust planning can. For example, if a spouse passes away, you could put a certain amount of your estate into a trust for the surviving spouse. That would protect the surviving spouse if they were to get remarried or have a creditor's claim or any type of Medicaid spend-down requirement. Portability wouldn't cover them. Another thing we see is that portability doesn't help protect your children's inheritance. If your children, for example, use proper trust planning, we could protect their inheritance from their creditors, predators, or failed marriages. Portability wouldn't do that. Portability also doesn't allow your heirs to lock in certain appreciation on assets the way traditional trust planning does. Finally, another issue we see with portability is that it doesn't help look for blended families. So, if you or your spouse have children from a prior relationship, portability wouldn't take care of that. You would want to have some sort of trust plan in...

Award-winning PDF software

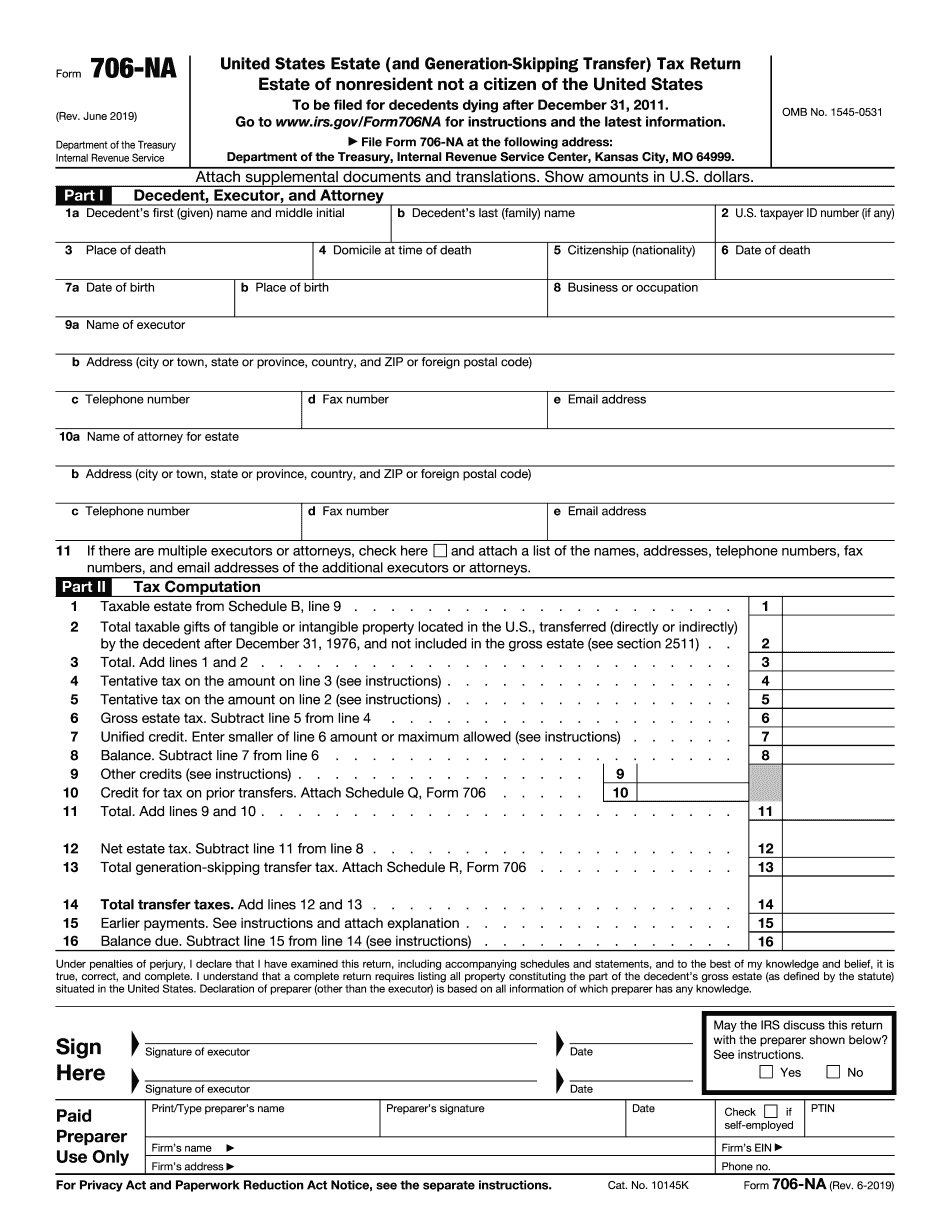

How to elect portability on 706 Form: What You Should Know

Portability must be timely filed. 5. The executor must include the statement required by section 4.01(2) of Rev. Pro. 2009-17 at the top of the Form 706.6. The executor must not file a tax return within a period specified by Sec. 482(a)(2) of the Code and, upon his or her death, the decedent's estate must file a tax return on the date established by Secs. 6012(a)(15)(H), (c)(3), and (c)(10). Instructions for Form 706 (10/15/17) ; IRS Instructions for Form 706 (10/15/17) Awarding estates tax on estate assets by a tax-free death, Form 706, is the most reliable method to ensure that the estate assets will be held in the state of the decedent's residence at death. It also affords the estate some flexibility in how it will invest the estate assets. These procedures were modified by a provision in the 2025 code which requires that the assets are to be distributed in accordance with Rev. Pro. 2016-29. “The Trustee shall hold and distribute to the beneficiaries the estate's net estate property in any amount determined by the court, including any income, capital gain, gains, interest, profits, and ordinary income that may be included in gross estate or payment. The court may approve a distribution which is larger than the minimum distribution required pursuant to the estate tax provisions. The court may also direct that no distributions be made.” [Emphasis added.] The Code specifies that the term “net estate property” includes all assets that are separate property. An executor can take advantage of this new opportunity for tax planning through the adoption or revocation of the estate's right to participate in a state or federal or a foreign income tax. If the deceased estate's right to participate in a federal or state tax is revoked, the decedent's assets can either be distributed to the estate and taxed as if the right had not been revoked or can be distributed to beneficiaries and taxed as ordinary income. It is important to note that the revocation of the right does not affect other provisions of state law applicable to the beneficiaries and their income. These provisions are discussed later.

Online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 706-Na, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 706-Na online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 706-Na by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 706-Na from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing How to elect portability on 706